The Homeowner's Freeze Claim Playbook

What insurance doesn't explain — and what experienced claim handlers know. A 10-part guide to freeze claims from prevention through final settlement.

The Homeowner's Winter Freeze Claim Playbook

Most of the damage from a winter freeze doesn't happen during the freeze. It happens after — when temperatures rise, water pressure returns, and pipes that cracked silently in the cold finally start leaking. By the time you see the water, the damage has often been spreading for hours.

That delayed discovery is normal. It's expected. What catches homeowners off guard isn't the timing — it's not knowing that insurance evaluates freeze claims on documentation and timelines, not just damage severity. This guide gives you the framework to navigate that process from day one.

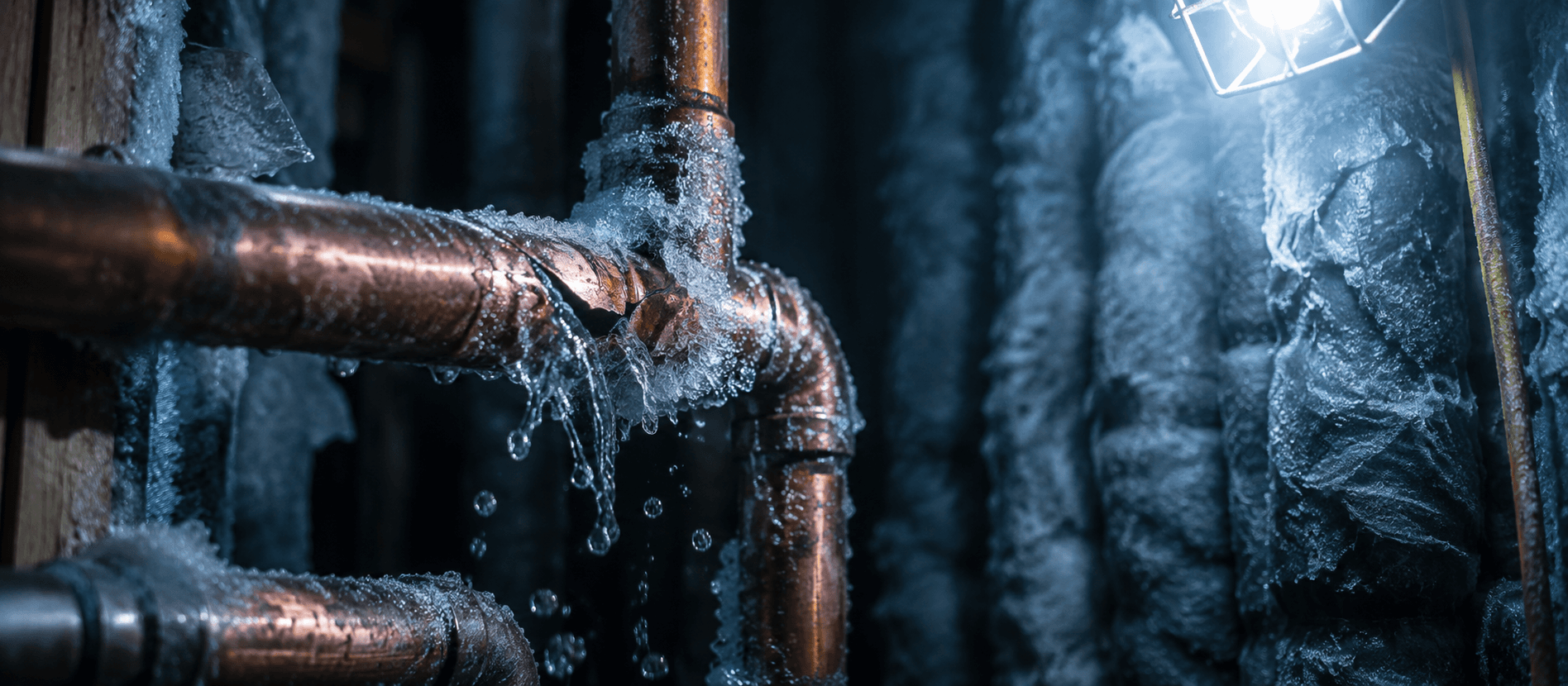

Why Do Freeze Claims Work Differently Than Other Water Damage Claims?

Freeze damage has a pattern that makes it uniquely complicated from an insurance standpoint: the failure event (freezing) and the discovery event (water appearing) are separated in time. Sometimes by hours. Sometimes by days.

Here's the mechanics: water inside a pipe freezes and expands, creating a crack or fracture. While the pipe stays frozen, nothing leaks — the ice itself is plugging the failure point. When temperatures rise and pressure returns, that's when the water starts moving. The crack that formed at 2 AM on Tuesday may not show itself until Thursday afternoon.

This matters for your claim because most homeowners policies cover damage that is "sudden and accidental." Adjusters are trained to determine whether damage resulted from a specific freeze event — or developed gradually over time due to pre-existing conditions or deferred maintenance. Delayed discovery is a well-understood pattern in freeze claims. Whether a specific loss is sudden and accidental is a coverage determination your insurer makes on your policy language and the evidence — which is why documenting the failure point and the timeline matters so much here.

What Is Your Insurer Actually Watching For?

Understanding the adjuster's evaluation framework helps you document the right things from the start.

Cause of loss — sudden vs. gradual. The central question in every freeze claim is whether the failure was caused by the freeze event or by a pre-existing condition. A pipe that was already corroded and slowly failing may not be covered. A structurally sound pipe that cracked due to thermal expansion during a freeze typically is. Adjusters look for: the location of the failure point, signs of long-term moisture versus fresh water damage, any prior leak history in the area, and consistency between your timeline and the weather records.

The heating question. Nearly every freeze adjuster will ask whether the heat was on and at what temperature. This isn't an accusation — it's a documented policy condition. Many policies require homeowners to maintain heat above a minimum threshold (often 55°F) to maintain freeze coverage. Know your policy's specific requirement and be accurate in your answer.

Pre-existing conditions. If there was prior damage, a known weak point, or a previous repair in the same area, adjusters note it. This doesn't automatically exclude coverage — but it becomes part of the evaluation.

Your job isn't to tell a perfect story. It's to document an accurate one. Consistency between your timeline, your photos, and your statements is what matters. Adjusters work from the overall picture, not individual pieces.

Common Reasons Freeze Claims Get Denied or Reduced

Failure to maintain heat. If your policy requires minimum indoor temperatures and the pipes froze in an unheated space, coverage may be limited or excluded. Vacation homes and investment properties are most vulnerable.

Pre-existing leak history. Prior plumbing issues in the same area create a question of whether the current damage is freeze-related or progressive deterioration. Document clearly that this area was dry before the freeze event.

Premature permanent repairs. If walls are closed and flooring replaced before the adjuster can inspect, the physical evidence for scope is gone. The adjuster can only pay for what they can verify — or what documentation clearly establishes.

Incomplete scope at settlement. Many freeze claims are settled before all damage is known — particularly hidden damage under floors and behind walls. Accepting a settlement before contractors have opened the structure often results in a final bill that exceeds the settled amount with no recourse.

Discarding damaged materials. Wet drywall and flooring are evidence. When materials are disposed of before the adjuster inspects, scope determinations rely on assumptions rather than direct assessment.

The Critical Window: Days 1-5

The first five days of a freeze claim determine more about the outcome than any other period. Here's what matters when.

Before anything else: photograph the source, not just the aftermath. Stained ceilings and wet floors matter less without a photo of the failure point — the cracked pipe, the burst fitting, the failed valve. Document the cause and the consequence. Wide shots to establish context, close-ups to show the failure. Capture the date and time in metadata by sending photos immediately — don't let them sit on your phone.

Extract water and start drying immediately. Mold growth becomes likely within 24-72 hours in wet materials. Water extraction and industrial drying equipment should start as quickly as possible — this is emergency mitigation, it's expected, and the costs are reimbursable under your dwelling coverage. Get itemized invoices from the restoration company: per-day equipment rates, labor hours, moisture readings at start and completion.

Document "no prior issues" statements while they're fresh. If this area had no prior leaks or known plumbing issues, say so in writing — in your claim notes, in a text to your contractor, in your initial claim filing. These statements are harder to reconstruct credibly three months later.

Notify your insurer within 24-48 hours. Get a claim number. Ask specifically: what is my ALE limit if the home becomes uninhabitable? Are emergency mitigation costs reimbursable? Who is my primary adjuster contact?

Hold off on permanent repairs until the adjuster has inspected — or until you have written authorization to proceed. Emergency mitigation (water extraction, temporary drywall removal to expose wet insulation, tarping) is appropriate. Replacement drywall, new flooring, and finished surfaces should wait. Once the structure is restored, the adjuster can only estimate what the documentation says was there.

Why the First Estimate Is Never the Full Picture

Insurance adjusters write their initial scope for visible, verified damage. They're not trying to estimate hidden damage before it's exposed — they can't, and most policies don't expect them to.

This is why the first insurance estimate often feels like it captures only half the damage. It often does. That's not a red flag — it's how the process is designed to work. As walls are opened and flooring is removed, additional damage becomes visible. Supplemental claims for that damage are normal, expected, and processed regularly.

The mistake is treating the first number as final. The homeowners who get caught are the ones who accept a settlement before contractors have opened the structure — before the hidden damage under the floors and behind the walls has been revealed. Once you've settled and closed the claim, that discovery has no recourse.

Before a claim is closed, have a licensed contractor walk the full scope of damage and get at least two independent estimates. Where a contractor documents damage categories the insurer's scope does not include, your policy's supplemental-claim provision is what covers work identified later — with contractor assessments and photos, not arguments to have verbally.

State-Specific Notes

Texas. Texas experienced catastrophic freeze events in 2021 that produced enormous claims volume and adjuster backlogs. Prompt payment is set by Tex. Ins. Code §§542.055–.058 (Prompt Payment of Claims Act) — acknowledge within 15 days (§542.055), accept/reject within 15 business days of receiving the items required for proof of loss (§542.056), pay within 5 business days of acceptance (§542.057). Verified as of 2026-07-20; confirm current law. If your insurer isn't meeting these timelines, the Texas Department of Insurance handles complaints at tdi.texas.gov.

Oklahoma and the Southern Plains. Freeze coverage disputes in this region frequently center on vacancy and heating requirements. Investment properties and second homes left unheated are the most common denial scenario. Verify your policy's heating requirement before a freeze event — retroactive documentation of thermostat settings is difficult.

Colorado and Mountain States. Elevation and older housing stock make freeze damage particularly common. Code upgrades triggered by repairs — particularly plumbing and electrical — may not be covered without an ordinance or law endorsement. If your home predates the 1990s, this endorsement is worth having.

All States. Acknowledgment and decision timelines are set by state regulation and vary — look up your state's rule rather than relying on a general range. When these timelines are exceeded, a formal complaint to your state insurance commissioner creates a record the insurer must respond to within a defined timeframe.

Frequently Asked Questions

My pipe froze but I'm not sure it's covered — what determines coverage? Coverage for freeze damage typically depends on two things: the cause of loss (the freeze itself must be the cause, not pre-existing deterioration) and your policy's conditions (most policies require minimum indoor heating temperatures to be maintained). If the heat was on and the pipe failed due to the freeze event, coverage is generally available. Document the heating situation and the timeline of discovery clearly.

Should I use the restoration company my insurer recommends? You're generally not required to use your insurer's preferred vendors. If you choose your own licensed restoration company, get itemized invoices — not lump-sum billing — and document the work with before-and-after photos. The coverage for mitigation costs is the same regardless of which licensed company performs the work.

The adjuster's estimate seems too low — what do I do? Compare the insurer's line-item estimate against your independent contractor estimates, specifically identifying items that appear in the contractor assessments but not in the insurer's scope. Missing line items — not just pricing differences — are the most common cause of underpayment in freeze claims. Request a re-inspection or submit a formal supplement with contractor documentation and photos of missed areas. Do not permanently repair those areas before the supplement is resolved.

How long do freeze claims typically take? Simple freeze claims with clear cause of loss and no hidden damage can resolve in 4-8 weeks. Claims that involve opening walls and discovering secondary damage routinely run 3-6 months. The factor that extends timelines most is unresolved supplemental damage — file supplements promptly as additional damage is discovered, rather than accumulating them for a single end-of-project submission.

What if damage keeps appearing weeks after the freeze? This is normal in significant freeze events — water travels under floors and through wall cavities before it's visible. Document each new area of damage as it's discovered: photos, date, description, and a note from your contractor connecting it to the original event. File a supplemental claim for each newly documented area. Don't wait until repairs are complete to report additional damage.

When should I consider a public adjuster for a freeze claim? A public adjuster is worth considering when the estimated damage is $50,000 or more, the insurer's scope is significantly below your contractor estimates and written disputes haven't moved it, or you don't have the time to manage a complex multi-month claim yourself. Public adjusters typically charge 10-15% of the settlement. Verify their license through your state's insurance department before signing anything.

Managing a freeze claim on your own is completely possible with the right documentation and organization. ClaimEase tracks every photo, expense, and communication connected to your claim record — so when a supplement needs to be filed for damage found in week six, you have the photos, the contractor notes, and the communication record that supports it. And when the settlement offer arrives, you can compare it against a complete documented loss rather than a rough recollection.

ClaimEase provides general guidance. Coverage determinations are made by your insurer based on your specific policy terms. Consult a licensed public adjuster or attorney for specific advice about your claim. State laws and policy terms vary.